Planning to buy a home, a car for family trips, or need quick funds for an emergency? Most loans come with EMI the fixed monthly payment that makes big purchases affordable over time.

But what exactly is EMI? How is it calculated? Why does your EMI stay the same while the interest portion drops? And how can you save thousands (or lakhs) on interest?

In this detailed guide, we cover everything: EMI meaning, full form, formula, step-by-step calculations, real examples for home/car/personal loans, amortization breakdown, prepayment benefits, common mistakes, and answers to the most searched questions. Plus, learn how to use a free EMI Calculator to plan smartly and avoid overpaying.

What Is EMI?

EMI stands for Equated Monthly Instalment, which is the fixed amount a borrower pays every month to the lender until the loan is fully repaid. This payment remains constant throughout the tenure (except in rare cases of floating rate adjustments), making budgeting predictable and straightforward for salaried individuals or business owners.

What is EMI in loans?

In loans, EMI represents your regular monthly commitment that covers both the repayment of the borrowed principal amount and the interest charged by the bank or NBFC, ensuring the entire debt is cleared by the end of the agreed period without any balloon payments at the end.

What does EMI stand for / What is EMI full form?

EMI full form is Equated Monthly Instalment “Equated” refers to the equal/fixed nature of each payment, “monthly” indicates the frequency, and “instalment” means it’s a partial repayment of the total loan obligation over time.

What is EMI in finance?

In the broader finance context, EMI is a standardised repayment structure widely adopted for retail loans like home, car, personal, education, and gold loans, promoted by major lenders such as SBI, HDFC, ICICI, Bajaj Finserv, and others to provide transparency, ease of planning, and widespread accessibility to credit for middle-class families.

How Does EMI Work?

EMI works on the principle of reducing balance interest calculation, where each monthly payment is split into two parts: one portion goes toward paying the interest accrued on the outstanding principal, while the remaining portion reduces the principal itself, gradually lowering the loan balance over time.

What is included in EMI (principal vs interest)?

Every EMI consists of interest (calculated on the current outstanding principal) and principal repayment; initially, a larger share covers interest because the balance is high, but as the principal decreases month after month, more of the EMI starts contributing to principal reduction, accelerating the debt payoff in later stages.

Why is interest higher in the beginning?

Interest is charged only on the remaining loan amount each month, so when the outstanding principal is at its maximum during the early tenure, the interest component is significantly larger; this front-loading of interest is a standard feature of most loans, ensuring lenders recover their profit early while still allowing borrowers to build equity gradually.

What is reducing balance method?

The reducing balance method (also called diminishing balance) is the most common EMI calculation approach, where interest is applied only to the outstanding principal after each payment, unlike the outdated flat-rate method that charges interest on the full original amount throughout. This makes reducing the balance more borrower-friendly, as total interest paid decreases over time.

What is amortisation in EMI?

Amortisation refers to the systematic reduction of the loan through scheduled payments; an amortisation schedule is a detailed table or chart that breaks down every EMI into its interest and principal components, shows the remaining balance after each payment, and helps borrowers visualise how their debt shrinks month by month until it reaches zero at the end of the tenure.

EMI Formula and Calculation

The standard mathematical formula for calculating EMI under the reducing balance method, used by all major banks and online tools, is:

EMI=(1+r)n−1P×r×(1+r)n

What are P, r, and n in EMI formula?

P stands for the principal loan amount (the money you actually borrow), r is the monthly interest rate (annual rate divided by 12 and then by 100), and n represents the total number of monthly instalments (loan tenure in years multiplied by 12), forming the three core variables that determine your fixed monthly payment.

How is EMI calculated?

EMI is computed by applying the formula above, which accounts for compounding interest on a monthly basis and ensures the total of all payments exactly covers the principal plus accumulated interest over the chosen tenure, providing a balanced repayment structure.

How to calculate EMI manually?

To calculate EMI manually, first convert the annual interest rate to monthly (divide by 12 and 100), compute (1 + r) raised to the power of n, then plug all values into the formula step-by-step; while possible with a scientific calculator, it’s time-consuming and prone to errors, which is why online EMI calculators or Excel’s PMT function are preferred for accuracy and speed in real-world scenarios.

How to Use EMI Calculator

An EMI calculator is a free, user-friendly online tool available on bank websites, financial portals like Groww, ClearTax, Policybazaar, and Bajaj Finserv, designed to instantly compute your monthly instalment and total repayment details.

How to calculate EMI using calculator?

Simply visit any reliable EMI calculator page, input the loan amount (principal), select or enter the annual interest rate offered by the lender, choose the repayment tenure in years or months, and click “Calculate” to get the exact EMI figure along with total interest payable and a full amortization preview.

What inputs are required (loan amount, interest, tenure)?

The three essential inputs are the principal loan amount you wish to borrow, the applicable annual interest rate (fixed or floating as quoted), and the desired loan tenure in years or months, which together allow the tool to apply the standard EMI formula accurately.

How accurate is EMI calculator?

EMI calculators are highly accurate because they use the precise mathematical formula employed by banks, though minor variations (a few rupees) may occur due to rounding rules, processing fees, or exact disbursement date; they provide reliable estimates for planning purposes.

Can EMI calculator be used for all loans?

Yes, these calculators work universally for home loans, car loans, personal loans, education loans, gold loans, and even business loans, with specialised versions sometimes offering additional fields like prepayment options or moratorium periods for education loans.

Factors Affecting EMI

Besides the principal amount and the rate of interest, there are several other factors that affect the EMI and the repayment structure for the loan.

Factors like interest rate, loan tenure, loan amount, fixed vs floating interest rate, and type of loan(home loan, Education loan, vehicle loan) may affect the loan and repayment highly. Here is the breakdown for better understanding:

How does interest rate affect EMI?

A higher interest rate directly increases the EMI amount because more of each payment goes toward interest rather than principal, meaning even a 1% rise can significantly raise your monthly outflow and total repayment cost over the loan life.

How does loan tenure affect EMI?

Extending the tenure lowers the EMI by spreading repayments over more months, making monthly payments more affordable, but it substantially increases the total interest paid since interest accrues for a longer period on the outstanding balance.

How does loan amount affect EMI?

A larger principal amount results in a proportionally higher EMI, as the formula scales directly with P; borrowing more means higher monthly commitments, so borrowers must balance their needs against realistic repayment capacity.

Fixed vs floating interest rate impact

Fixed-rate loans keep the EMI constant throughout the tenure for predictable budgeting, while floating-rate loans (linked to repo rate or MCLR) may cause EMI fluctuations if benchmark rates change, though many Indian banks prefer adjusting tenure to maintain the same EMI level for customer convenience.

EMI Calculation Examples

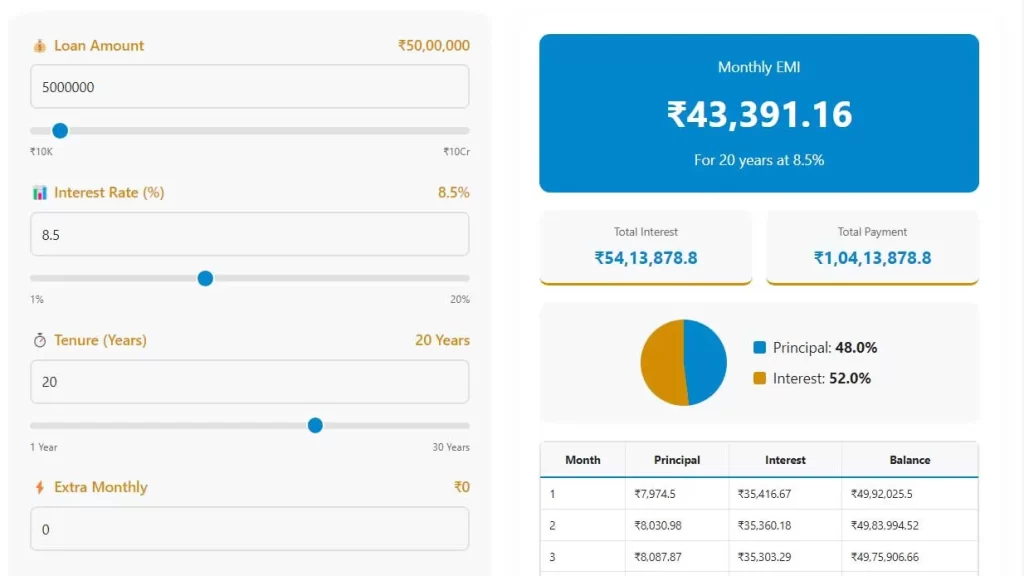

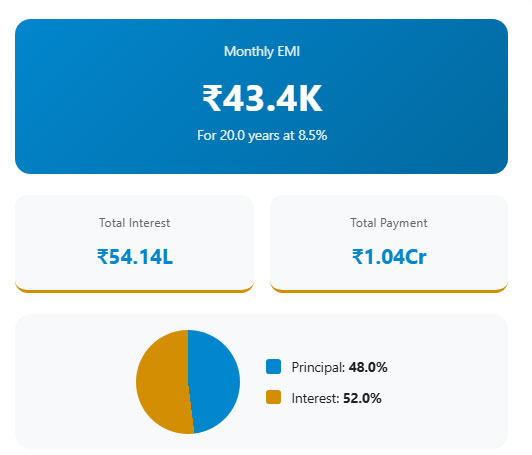

Example of home loan EMI calculation For a ₹50 lakh home loan at 8.5% p.a. interest with a 20-year (240 months) tenure, the EMI calculates to approximately ₹43,391 per month using the standard formula; over the full period, you repay about ₹1.04 crore total, with roughly ₹54 lakh going toward interest, highlighting the long-term cost of borrowing for property in areas like Dhanbad.

Example of car loan EMI

A ₹10 lakh car loan at 9% p.a. for 5 years (60 months) results in an EMI of around ₹20,758 monthly; the total repayment reaches approximately ₹12.45 lakh, including ₹2.45 lakh in interest, which is typical for vehicle financing where shorter tenures help control overall costs.

Example of personal loan EMI

For a ₹5 lakh personal loan at 12% p.a. over 3 years (36 months), the EMI comes to about ₹16,607 per month; total interest paid is roughly ₹97,852, reflecting the higher rates and shorter tenures common in unsecured personal loans used for emergencies or weddings.

EMI Breakdown (Principal vs Interest)

What is EMI amortisation schedule?

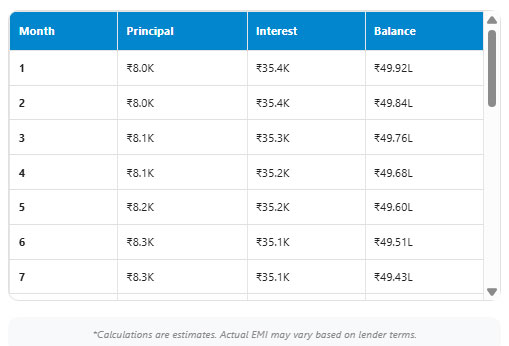

An amortisation schedule is a comprehensive month-by-month table provided by lenders or generated via calculators, detailing how each EMI is divided between interest and principal, the outstanding balance after each payment, and the gradual shift toward principal-dominant repayments.

Monthly EMI breakdown example

In the early months of a ₹50 lakh home loan at 8.5%, the first EMI might allocate ₹35,417 to interest and only ₹7,974 to principal, but by the midpoint (around month 120), interest drops to about ₹20,000 while principal repayment rises to ₹23,391, demonstrating the accelerating equity build-up.

Interest vs principal over time:

Interest forms the majority (often 60–80%) of EMI in the initial years when the principal is highest, but it steadily declines as the outstanding balance reduces; by the final years, principal repayment dominates (80–90%+), ensuring the loan is fully cleared with minimal interest in the closing stages.

How EMI changes month to month:

While the total EMI remains fixed, the internal composition shifts dynamically interest portion decreases gradually with each principal reduction, allowing more of the fixed payment to chip away at the debt, creating a snowball effect in debt clearance toward the end.

EMI vs Loan Tenure & Interest

Short tenure vs long tenure EMI Opting for a shorter tenure results in a significantly higher EMI but dramatically lowers total interest paid because the principal is repaid faster with less time for interest to accumulate; conversely, a longer tenure reduces monthly pressure but inflates overall cost substantially.

Which is better: high EMI or low EMI?

High EMI with shorter tenure is financially superior if your income allows it, as it minimises interest outflow and builds ownership equity quicker; low EMI suits those with tighter budgets but comes at the expense of paying much more in total interest over time.

Total interest vs EMI tradeoff

For a ₹50 lakh loan at 8.5%, a 10-year tenure might demand EMI around ₹61,000+ with total interest of about ₹23 lakh, while stretching to 20 years lowers EMI to ₹43,000 but pushes total interest to ₹54 lakh, illustrating the clear tradeoff between monthly affordability and long-term savings.

Prepayment and EMI Reduction

What happens if you prepay loan?

Making a lump-sum prepayment directly reduces the outstanding principal, which in turn lowers future interest calculations since interest is charged only on the remaining balance, leading to substantial savings and potentially earlier loan closure.

How prepayment reduces interest.

Each rupee prepaid eliminates interest that would have otherwise accrued on that amount for the remaining tenure, effectively giving you a risk-free return equal to the loan interest rate; partial prepayments early in the tenure yield the highest savings due to the front-loaded interest structure.

EMI vs tenure reduction options.

After prepayment, most Indian banks offer two choices: reduce the EMI while keeping the original tenure (easing monthly cash flow) or shorten the tenure while maintaining the same EMI (maximising interest savings and faster debt freedom). The latter is generally more beneficial long-term.

How much interest can you save?

Prepaying ₹5 lakh early on a ₹50 lakh home loan could save ₹10–15 lakh in interest and shorten the tenure by 3–5 years or more, depending on timing and remaining balance, making regular partial prepayments one of the smartest ways to cut borrowing costs.

Types of EMI Calculators

Home loan EMI calculator: handles longer tenures (15–30 years) and higher amounts (₹20 lakh–₹1 crore+), often including features like prepayment simulation and tax benefit previews for properties.

Car loan EMI calculator: focuses on moderate amounts (₹5–25 lakh) and shorter tenures (3–7 years), with quick comparisons across vehicle financiers offering competitive rates.

Personal loan EMI calculator: caters to unsecured, higher-rate (10–24% p.a.) loans with short tenures (1–5 years), emphasizing instant results for emergency or consumption needs.

Education loan EMI calculator: incorporates special features like moratorium periods (course duration + 6–12 months) where only interest or no payments are due initially, common for higher studies or abroad.

Advantages of EMI Calculator

EMI calculators provide instant, error-free computations that save time compared to manual formula application, allowing you to experiment with different scenarios without any cost or commitment.

They enable side-by-side comparison of loan offers from multiple banks, helping identify the most affordable option based on EMI, total interest, and tenure flexibility for better financial decision-making.

By revealing the full repayment picture upfront, including total interest and amortisation, these tools support realistic budgeting, prevent over-borrowing, and promote responsible debt management in everyday Indian households.

Common Mistakes in EMI Calculation

Ignoring processing fees: Many borrowers calculate EMI based only on principal and rate, overlooking one-time fees (0.5–2%) or insurance charges that increase the effective loan amount and actual outflow.

Not considering floating rates: Assuming fixed EMI forever on floating-rate loans can lead to surprises if repo/MCLR rises, causing higher payments or extended tenure unless you factor in potential rate changes during planning.

Overestimating repayment capacity: Focusing solely on low EMI without accounting for other expenses, inflation, or job risks often results in defaults; always keep EMI below 35–40% of take-home salary for safety.

Focusing only on EMI, not total cost: Choosing the lowest EMI by extending tenure ignores massive interest accumulation; smart borrowers always review total payable amount alongside monthly outflow.

Frequently Asked Questions

How can I calculate my EMI?

The easiest and most accurate way is to use a free online EMI calculator by entering your loan amount, current interest rate, and desired tenure in months or years; alternatively, apply the standard formula manually with a calculator, though online tools are faster and less error-prone for most people.

Can EMI change over time?

For fixed-rate loans, EMI remains unchanged throughout the tenure for complete predictability; however, in floating-rate loans (common for home loans), EMI may increase or decrease if benchmark rates change, though many banks adjust tenure instead to keep EMI stable and avoid shocking borrowers.

What is a good EMI amount?

A good EMI is typically 30–40% of your monthly take-home salary to leave sufficient buffer for living expenses, emergencies, savings, and investments; going beyond 50% risks financial strain, especially with rising costs or unexpected events.

Does EMI include GST?

EMI itself usually does not include GST, as GST (18%) applies separately to processing fees, interest portions in some cases, or insurance; these taxes are either added upfront to the loan amount or billed separately, so check the sanction letter for the exact breakdown.

How to reduce EMI amount?

You can reduce EMI by making lump-sum prepayments to lower the principal (then opting for EMI reduction), refinancing the loan at a lower interest rate from another lender, or extending the tenure if allowed prepayment combined with tenure reduction often saves the most overall.

Can I increase EMI later?

Yes, most banks permit voluntary EMI increases or step-up options to accelerate repayment and reduce total interest; you can also make regular partial prepayments without changing EMI, which shortens tenure automatically and cuts interest significantly.

What happens if EMI is missed?

Missing an EMI triggers late payment penalties (typically 2–4% of EMI), additional interest on overdue amount, negative impact on CIBIL credit score (making future loans costlier or harder), and potential legal recovery actions if defaults continue. Always prioritise timely payments.

Is EMI same for all loans?

No, EMI varies greatly depending on loan type: home loans have lower EMIs due to lower rates and longer tenures, car loans are moderate, while personal loans have higher EMIs because of elevated interest rates and shorter repayment periods for the same borrowed amount.

Conclusion

EMI is the cornerstone of responsible borrowing, transforming large expenses into manageable monthly commitments through a balanced mix of principal and interest under the reducing balance system. Mastering how EMI is calculated via the standard formula, amortisation dynamics, and key influencing factors like rate and tenure empowers you to choose optimal loan terms, avoid excessive interest, and maintain healthy finances.

Before applying for any loan, whether for a home, a family car, or personal needs, always run multiple scenarios through a reliable EMI calculator to assess affordability, compare lenders, and simulate prepayments for maximum savings.

Smart planning with EMI knowledge not only secures your dreams but also protects your long-term financial health. Start using an EMI calculator today, borrow wisely, and enjoy the peace that comes with informed decisions.

Happy borrowing (and repaying smarter)!