If you are new to investing, you have probably heard people throw around terms like stocks, bonds, mutual funds, and ETFs. It can feel overwhelming at first.

But here is the truth: these four investment types are actually quite simple once you understand the basic idea behind each one.

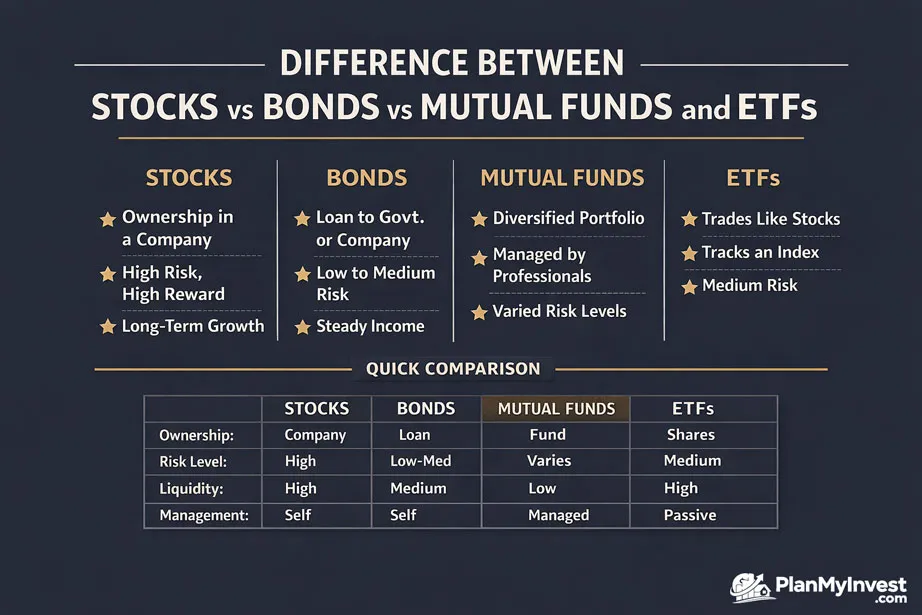

The main difference between stocks, mutual funds, ETFs, and bonds comes down to what you actually own and how that ownership works.

Stocks mean you own a piece of a company. Bonds mean you have lent money to someone. Mutual funds and ETFs are like baskets that hold many stocks or bonds together.

Difference Between Stocks, Bonds, Mutual Funds, and ETFs

Stocks represent company ownership. Bonds are loans to governments or corporations. Mutual funds pool money across investments and price once daily. ETFs pool money like mutual funds but trade throughout the day like stocks. Each serves a different role in a balanced portfolio.

Understanding the difference between these investment vehicles is the first step to building wealth.

Each type plays a different role in a well-rounded portfolio. Some focus on growth. Some focus on steady income. Some offer a mix of both.

What Are Stocks and How Do They Work?

Stocks represent partial ownership in a company. When you buy a stock, you become a shareholder, which means you own a small part of that business.

If the company performs well, investors may benefit from price appreciation and sometimes dividends.

Stocks can be rewarding, but they can also move up and down quickly. Their prices depend on business earnings, market trends, interest rates, news, and investor sentiment.

That is why stocks are usually considered higher-risk investments than bonds and many diversified funds.

Think of it this way. If you buy a share of Apple or Microsoft, you literally own a tiny slice of that company.

You get to benefit when the company does well. If the company’s profits grow and more people want to buy its stock, the price goes up.

You can then sell your shares for more than you paid.

A simple example helps here. If a company grows profits and expands successfully, its stock price may rise because more investors want a piece of it.

This makes stocks a better fit for people who can handle short-term volatility in exchange for long-term growth potential.

If the business struggles, the share price may fall just as fast.

Stocks are traded on exchanges like the New York Stock Exchange or Nasdaq during market hours.

You can buy and sell them anytime the market is open.

The price changes constantly based on supply and demand, company performance, and broader economic conditions.

Here is what you need to know about risk. Stocks can lose value quickly.

In 2008, the stock market fell by nearly 40 percent.

In 2020, it dropped about 30 percent in a matter of weeks. But over long periods like 10 or 20 years, stocks have historically delivered higher returns than any other major asset class.

Stocks are best for people with a long time horizon who can handle short-term ups and downs.

If you are investing for retirement that is 20 or 30 years away, stocks should probably be a big part of your plan.

What Are Bonds and How Are They Different From Stocks?

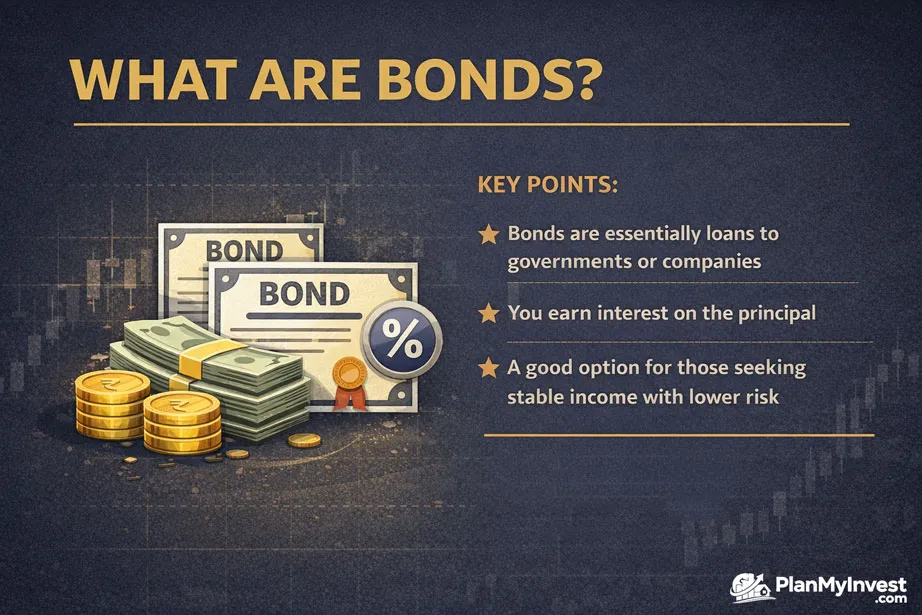

Bonds are debt instruments. When you buy a bond, you are lending money to a government, company, or other issuer in exchange for interest payments.

At maturity, the issuer usually returns the principal amount, assuming there is no default.

Bonds are often seen as more stable than stocks because they usually provide fixed or predictable income. That does not mean they are risk-free, though.

Bond prices can fall when interest rates rise, and the issuer may fail to repay the debt in rare cases.

Different types of bonds serve different purposes. Government bonds are generally considered safer, while corporate bonds may offer higher yields in exchange for more credit risk.

For many investors, bonds act as a stabilizer inside a portfolio that also includes stocks or funds.

Each investment type plays a different role. Stocks are focused on ownership and growth potential.

Bonds are focused on income and relative stability. Mutual funds and ETFs are built for diversification and convenience.

Bonds act like the steady part of your money. You’re the lender, not the owner.

If the issuer stays healthy, you get paid on schedule. Government bonds (especially U.S. Treasuries) are seen as very safe.

Corporate bonds pay a bit more interest but carry a slightly higher risk of default.

Municipal bonds often come with tax advantages that make them attractive for people in higher tax brackets.

Here is a simple way to think about them. If you want high upside and can tolerate volatility, stocks may fit.

If you want professional management and broad exposure, mutual funds may work well.

If you want similar diversification with lower costs and intraday trading, ETFs may be appealing.

If you want a steadier income and lower price swings, bonds may be the better fit.

Compared with stocks, bonds usually deliver lower returns over time but shine when markets get choppy.

They’re the counterbalance that keeps a portfolio from swinging wildly.

What are mutual funds, and why do investors use them?

A mutual fund pools money from many investors to buy a basket of stocks, bonds, or other assets. Professional managers make the investment decisions.

You buy and sell shares at the fund’s end-of-day price.

Imagine you want to own a diversified portfolio of 100 different stocks.

Buying each one individually would require a lot of money, time, and research.

With a mutual fund, you buy one share of the fund, and that share represents a tiny piece of all 100 stocks.

Professional money managers run mutual funds. These managers decide which stocks or bonds to buy and sell.

They do the research and make the trades. You just put your money in and let them handle the rest.

There are two main types of mutual funds. Actively managed funds have a team of analysts and managers trying to beat the market. They pick stocks they believe will perform well.

Passively managed funds, also called index funds, simply try to match the performance of a market index like the S&P 500.

They do not try to beat the market. They just follow it.

Here is an important detail about mutual funds. They price only once per day, after the market closes.

When you place an order to buy or sell mutual fund shares, that trade executes at the next available price.

You cannot trade mutual funds throughout the day like you can with stocks or ETFs.

Mutual funds often have minimum investment requirements. Some funds require $1,000 or even $10,000 to start.

But many funds have lowered their minimums, and some index funds from companies like Vanguard and Fidelity have no minimum at all.

Who should consider mutual funds?

They are great for beginners who want professional management without picking individual stocks.

They are also ideal for retirement accounts where you plan to hold for the long term and do not need to trade frequently.

Many people choose mutual funds because they are simple and diversified. Instead of researching dozens of companies, you can buy one fund and get exposure to a broad portfolio.

This makes mutual funds useful for beginners, long-term investors, and people who want a hands-off approach.

Mutual funds can be actively managed or passively managed. Actively managed funds try to beat the market, while index funds try to match a market benchmark.

They are usually priced once a day after the market closes, and many require a minimum investment amount.

What makes mutual funds different from buying individual assets?

Mutual funds pool money from many investors to buy a diversified mix of stocks, bonds, or both.

A professional manager (or an index) chooses the holdings, and you own shares in the fund rather than the underlying securities.

This gives built-in diversification without you having to research dozens of companies yourself.

Mutual funds were the original “set it and forget it” option for regular investors. Instead of picking ten stocks, you buy one fund that might hold hundreds.

They trade only once per day at the net asset value (NAV) calculated after the market closes.

Many are actively managed, meaning the team tries to beat the market, though plenty of low-cost index mutual funds simply track an index like the S&P 500.

The big advantage is professional oversight and easy diversification.

The trade-off is that you pay an expense ratio, typically 0.5% to 1% per year, and you don’t control exactly which stocks or bonds sit inside.

Mutual Fund Calculator-Calculate your return

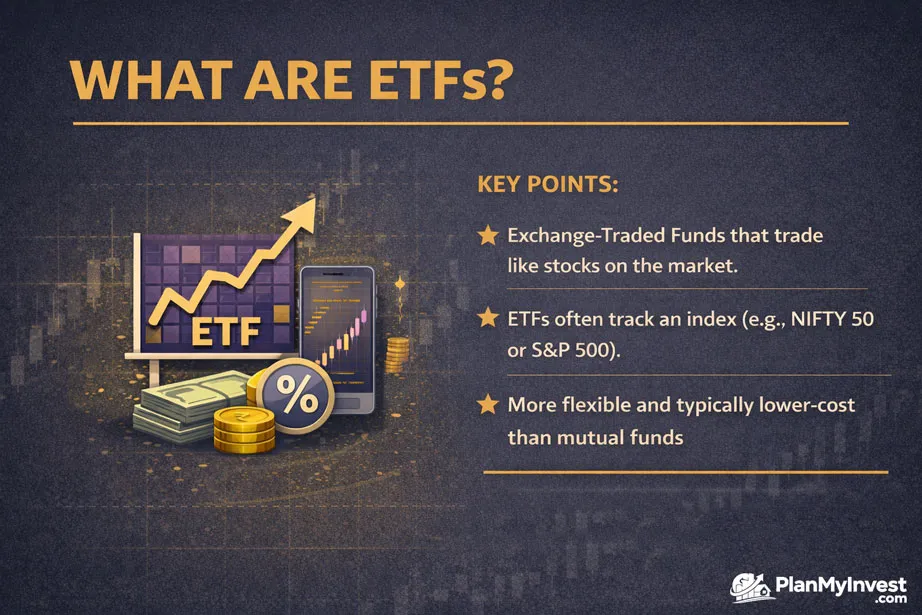

What Are ETFs and How Do They Compare to Mutual Funds?

An ETF (exchange-traded fund) holds a basket of investments like a mutual fund but trades on stock exchanges throughout the day like a stock. ETFs typically have lower fees and better tax efficiency than mutual funds.

This is the key difference between mutual funds and ETFs. Both give you a diversified basket of investments. Both can track the same indexes or focus on the same sectors. But the way you buy and sell them is completely different.

ETFs are more tax-efficient. The creation and redemption process allows ETFs to avoid triggering capital gains taxes for shareholders.

Mutual funds frequently distribute capital gains at year’s end, even if you did not sell any shares. For taxable accounts, ETFs are usually the smarter choice.

Mutual funds offer some advantages too. You can buy fractional shares of mutual funds easily. You can set up automatic monthly investments.

You do not have to worry about bid-ask spreads or trading commissions (though many brokers now offer commission-free ETF trading).

For retirement accounts like 401(k) plans and IRAs, mutual funds are often the only option available. For taxable brokerage accounts, ETFs are usually the better choice.

How do ETFs generate income?

Bonds are debt instruments. When you buy a bond, you are lending money to a government, company, or other issuer in exchange for interest payments.

At maturity, the issuer usually returns the principal amount, assuming there is no default.

Bonds are often seen as more stable than stocks because they usually provide fixed or predictable income.

That does not mean they are risk-free, though. Bond prices can fall when interest rates rise, and the issuer may fail to repay the debt in rare cases.

Different types of bonds serve different purposes. Government bonds are generally considered safer, while corporate bonds may offer higher yields in exchange for more credit risk.

For many investors, bonds act as a stabilizer inside a portfolio that also includes stocks or funds.

How are stocks, mutual funds, ETFs, and bonds compare?

Each investment type plays a different role. Stocks are focused on ownership and growth potential.

Bonds are focused on income and relative stability. Mutual funds and ETFs are built for diversification and convenience.

Here is a simple way to think about them. If you want high upside and can tolerate volatility, stocks may fit.

If you want professional management and broad exposure, mutual funds may work well.

If you want similar diversification with lower costs and intraday trading, ETFs may be appealing.

If you want a steadier income and lower price swings, bonds may be the better fit.

Here is a comparison table that may help you with a better understanding:

| 🟢 Stocks | 🔵 Bonds | 🟡 Mutual Funds | 🟣ETFs |

|---|---|---|---|

| Represents ownership in a company | Essentially a loan you give to a government or company | A pool of money managed by professionals | Similar to mutual funds but trade like stocks on exchanges |

| Returns: Capital gains + dividends | Returns: Fixed interest payments | Invests in stocks, bonds, or both | Usually tracks an index (like Nifty 50 or S&P 500) |

| Risk: High | Risk: Low to medium | Returns: Based on fund performance | Returns: Market-based |

| Best for: Long-term growth | Best for: Stable income | Risk: Varies (low to high) | Risk: Medium |

| 👉 Example: Buying shares of a company like Reliance or Apple | 👉 Example: Government bonds or corporate bonds | 👉 Good for beginners who want diversification without picking stocks | 👉 More flexible and often lower fees than mutual funds |

Which Investment Is Right for a Beginner?

This is the big confusion for beginners who are willing to start their investment journey.

If you are just starting out, mutual funds and ETFs are almost always better than picking individual stocks. Here is why.

When you buy individual stocks, you are betting that a specific company will do well. Even professional investors get this wrong all the time.

A diversified fund spreads your money across dozens or hundreds of companies. That way, if one company has a bad year, the others can pick up the slack.

The difference between buying a stock and buying a fund is the difference between betting on one horse and buying a small piece of every horse in the race. The diversified approach is much safer, especially for beginners.

For someone with a small amount to invest, say $500 or $1,000, an ETF is often the best choice.

You can buy one share of a broad market ETF like VTI (total stock market) or SPY (S&P 500) and instantly own a piece of thousands of companies. The fees are tiny, and you do not need to do any research.

If you prefer a hands-off approach where money is automatically invested from your paycheck, a mutual fund might be better.

Many mutual funds allow automatic investments of as little as $50 or $100 per month. That makes saving and investing effortless.

Avoid trying to time the market or pick winning stocks when you are starting out. The data is clear.

Most professional stock pickers do not beat the market over long periods. You certainly will not either.

Stick with low-cost diversified funds and focus on how much you save, not which stocks you pick.

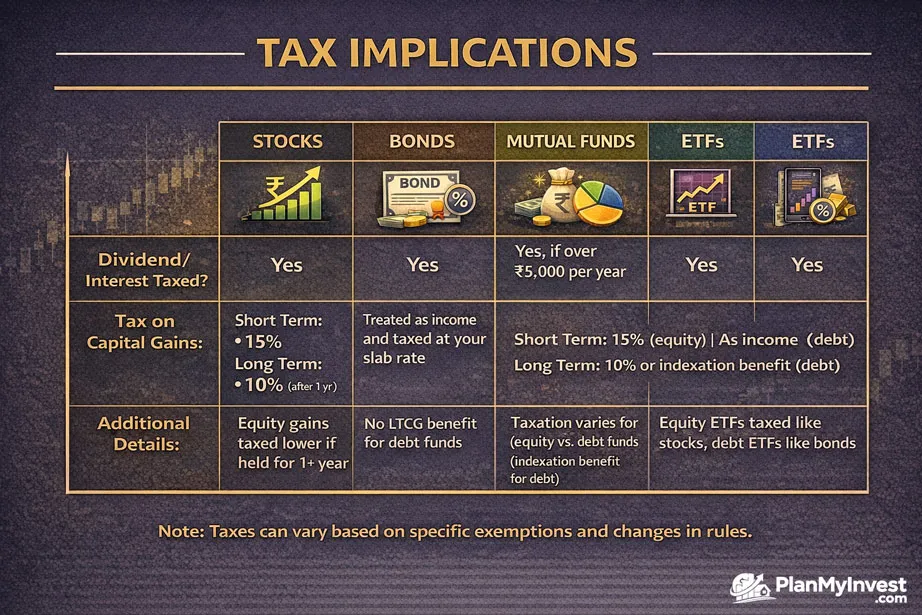

Tax Differences Between Stocks, Bonds, Mutual Funds, and ETFs

Taxes matter more than most beginners realize. The difference between an ETF and a mutual fund in a taxable account can be thousands of dollars over a decade.

Stocks and ETFs are generally more tax-efficient than mutual funds. When you hold a stock or ETF, you only pay capital gains tax when you sell your shares. You control the timing. You can hold for over a year to get the lower long-term capital gains rate.

Mutual funds are different. Even if you do not sell any shares, the fund itself might sell holdings during the year and generate capital gains.

Those gains get distributed to all shareholders, including you. You pay tax on those gains even though you never received cash from a sale. This is called a phantom tax bill.

Bonds generate interest income, which is taxed as ordinary income. This is less favorable than qualified dividends from stocks or long-term capital gains.

For this reason, bonds are often best held in tax-advantaged accounts like IRAs(Inland Revenue Authority of Singapore) or 401(k)s(employer-sponsored retirement savings plan in the U.S).

ETFs largely avoid the phantom capital gains problem through a process called in-kind creation and redemption.

This structural advantage makes ETFs significantly more tax-efficient than mutual funds for taxable accounts.

If you are investing in a retirement account like a 401(k) or IRA, these tax differences do not matter. In those accounts, all growth is tax deferred regardless of what you hold. But for regular taxable brokerage accounts, the difference between ETF and mutual funds is very real.

How can you build a balanced portfolio?

A balanced portfolio usually combines multiple asset types instead of relying on just one. Stocks may provide growth, mutual funds and ETFs may provide diversification, and bonds may provide income and stability.

This mix can help reduce the damage from market swings.

Your allocation should depend on your age, goals, income needs, and ability to handle losses.

A younger investor with a long timeline may lean more toward stocks and equity funds. Someone near retirement may prefer a larger bond allocation to reduce volatility.

The point is not to find one perfect investment. The goal is to use the strengths of each one in a way that supports your financial plan.

That is often more effective than trying to predict which asset will be the best performer every year.

Frequently Asked Questions

Which is better for monthly investing, ETF or mutual fund?

Mutual funds are often better for monthly automatic investing. Most brokers allow you to set up automatic purchases of mutual funds for as little as $50 or $100 per month. ETF automatic investing is less common, though some brokers now offer it.

Do I need to own all four types?

No. Many investors do just fine with only ETFs or only mutual funds. You do not need individual stocks at all. A simple portfolio of two or three ETFs or mutual funds can be perfectly adequate for most people.

What is the difference between an index fund and an ETF?

An index fund is a type of investment that tracks a market index. Index funds can be structured as either mutual funds or ETFs. So an ETF is one type of index fund. Not all mutual funds are index funds. Many are actively managed.

Are bonds safer than dividend stocks?

Generally yes. Bond interest payments are contractually obligated. Dividends can be reduced or eliminated at any time. But dividend stocks offer potential for price appreciation. The difference between a bond and a dividend stock is the difference between a loan and an ownership stake.

How are ETFs and mutual funds different in terms of fees?

ETFs almost always have lower expense ratios than comparable actively managed mutual funds. For passive index funds, the difference is smaller but still favors ETFs. You will also find that ETFs have no sales loads, while some mutual funds charge front-end or back-end loads.

Can I hold ETFs and mutual funds in the same account?

Yes. Most brokerage accounts allow you to hold both. You can mix and match based on which type works best for each part of your portfolio.

Which investment type has the highest historical returns?

Stocks have the highest historical returns by a wide margin. Over the past century, U.S. stocks have returned about 10 percent annually on average. Bonds have returned about 5 percent. Cash has returned about 3 percent.

Are ETFs better than mutual funds?

ETFs are often cheaper and more flexible because they trade during the day. Mutual funds may be better if you prefer automatic investing, active management, or traditional fund structures. The better choice depends on your goals and investing style.

Are stocks riskier than bonds?

Yes, in general stocks are riskier than bonds. Stocks can deliver higher long-term growth, but they can also swing more sharply in the short term. Bonds usually provide steadier income and less price volatility.

Can mutual funds invest in both stocks and bonds?

Yes, many mutual funds invest in a mix of stocks and bonds. These are often called balanced funds or hybrid funds. They are designed to provide diversification in a single product.

What is the main advantage of ETFs?

The main advantage of ETFs is that they combine diversification with trading flexibility and often lower costs. You can buy or sell them throughout the trading day, just like stocks. That makes them appealing to many long-term and active investors.

What is the safest investment among these four?

Bonds are generally considered safer than stocks, mutual funds, and ETFs, but they are not risk-free. The safest choice depends on the type of bond, the issuer, and the investor’s goal. Safety should always be balanced against inflation and return needs.

Should beginners start with stocks or mutual funds?

Many beginners start with mutual funds or ETFs because they are easier to understand and more diversified. Individual stocks can come later once the investor is comfortable with research and market volatility. Starting simple usually helps build confidence.

Conclusion:

Stocks, mutual funds, ETFs, and bonds all serve different roles in investing. Stocks are for ownership and growth, bonds are for income and stability, and mutual funds and ETFs are for diversification and convenience.

If you understand the difference between them, you can choose investments based on your goals instead of guesswork. That is the real advantage of learning these basics early.