Every investor eventually faces the same confusion: “My mutual fund app shows 12% returns, but my SIP statement says 15% — which one is real?”

That confusion comes from two powerful but very different metrics: CAGR and XIRR.

CAGR (Compound Annual Growth Rate) is the simple, smooth number everyone loves for lump-sum investments. XIRR (Extended Internal Rate of Return) is the realistic, cash-flow-aware number that SIP investors in India actually need.

In this ultimate guide, we break down CAGR vs XIRR with real examples, clear formulas, Excel steps, detailed comparison tables, pros & cons, and answers to the 8 most common questions people ask on Google, Quora, and mutual fund forums. By the end, you’ll know exactly which metric to use — and never get fooled by wrong return numbers again.

What Is CAGR?

CAGR stands for Compound Annual Growth Rate.

It measures the average annual growth of a single investment over a fixed period, assuming the money compounds steadily every year with no additional deposits or withdrawals.

CAGR is the “what-if” rate: “If I had invested the entire amount on day one and it grew smoothly, what constant yearly return would I get?” Although CAGR can be misleading for SIP when calculating the monthly investment.

It is the most popular metric for reporting long-term performance of stocks, indices, and lump-sum mutual fund investments because it is simple, comparable, and smooths out market volatility. Follow a detailed guide to learn about CAGR and calculations.

What Is XIRR?

XIRR stands for Extended Internal Rate of Return.

It is the actual annualized return you personally earned when you made multiple investments or withdrawals at different dates (like monthly SIPs, top-ups, or partial redemptions).

XIRR considers the exact amount and exact date of every cash flow, solving for the single rate that makes the net present value of all transactions zero.

In short: CAGR is about the investment. XIRR is about your money and your timing.

Key Differences Between CAGR and XIRR

| Feature | CAGR | XIRR |

|---|---|---|

| Full Form | Compound Annual Growth Rate | Extended Internal Rate of Return |

| Cash Flows | Single lump-sum (one investment, one exit) | Multiple & irregular (SIP, top-ups, withdrawals) |

| Timing Considered? | No (only start & end date) | Yes (every single date matters) |

| Best For | Lump-sum investments, stock performance, fund benchmarking | SIPs, staggered investments, real investor returns |

| Calculation Complexity | Very simple (manual or Excel) | Requires Excel or calculator (iterative) |

| Accuracy for SIP | Often misleading (overstates returns) | Most accurate & realistic |

| Mutual Fund Apps | Used for fund-level 1Y/3Y/5Y/10Y returns | Used for your personal portfolio/SIP returns |

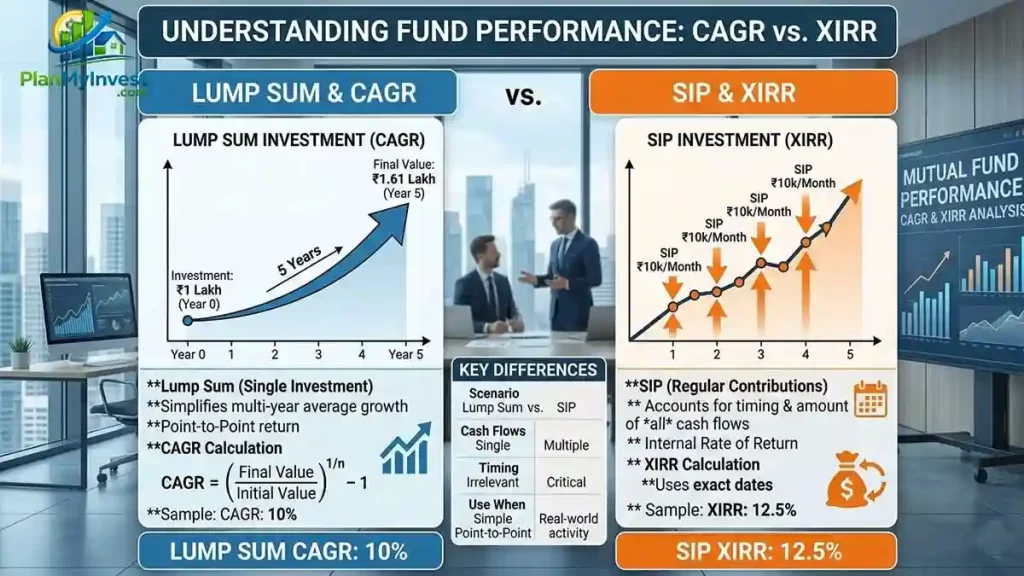

Real Example (2026 data style) You invest ₹1 lakh lump sum on 1 Jan 2021 → value becomes ₹2.1 lakh on 31 Dec 2025 (5 years). CAGR = 16%

Same fund, but you do ₹5,000 monthly SIP for 5 years (total invested ₹3 lakh) → final value ₹4.8 lakh. CAGR (wrong method) might show ~12% XIRR (correct) = 15.8% — because later installments had less time to grow.

When to Use CAGR vs XIRR

So, the big question, when to use CAGR and where XIRR give the real results.

Use CAGR When:

- You made a one-time lump-sum investment

- Comparing two different mutual funds or stocks over the same period

- Reading fund factsheets (1Y, 3Y, 5Y, 10Y returns)

- Calculating business revenue growth or stock performance

Use XIRR When:

- Investing via SIP (most common in India)

- Making irregular top-ups or step-up SIPs

- Withdrawing money at different times (SWP)

- Checking your actual personal return in Groww, Zerodha Coin, or Kuvera

Rule of Thumb: If your money went in at different times → use XIRR. If money went in once → use CAGR.

CAGR vs XIRR-Formula

CAGR Formula

CAGR=(Initial ValueFinal Value)Years1−1

Simple for beginners: Turn the ratio into a power of 1/Years and subtract 1.

XIRR Formula

There is no simple algebraic formula for XIRR. It is solved using iteration (trial & error) until the net present value becomes zero.

In Excel/Google Sheets: =XIRR(values, dates, [guess])

- values: column of cash flows (investments as negative, final value as positive)

- dates: exact dates of each transaction

- guess: optional (usually 0.1 or leave blank)

How to Calculate CAGR (Step-by-Step)

- Note initial investment (₹10,000)

- Note final value (₹25,000)

- Note exact years (5.5 years)

- Apply formula → CAGR ≈ 20.1%

How to Calculate XIRR in Excel (Step-by-Step with Example)

SIP Example (most common question): You invest ₹5,000 every month for 12 months. Final value ₹68,000.

Create Excel table:

You can also use this XIRR Calculator and download the result in PDF format.

CAGR vs XIRR in Mutual Funds & SIPs

When evaluating the performance of your mutual fund investments, you will frequently encounter two key metrics: CAGR (Compound Annual Growth Rate) and XIRR (eXtended Internal Rate of Return).

Understanding the difference between them is crucial, as using the wrong one can lead to a significant misinterpretation of your actual returns.

The Core Difference

The fundamental distinction lies in how they handle the timing and frequency of your investments.

- CAGR (Compound Annual Growth Rate) is a standard measure of average annual growth between two specific points in time. It assumes a single, one-time investment made at the start and completely withdrawn at the end.

It smooths out market volatility, providing a single percentage that represents what your annual return would have been if the growth had been constant. - XIRR (eXtended Internal Rate of Return) is a more precise calculation that accounts for the actual timing and amount of every single cash flow—every SIP installment, lump sum addition, and withdrawal.

It recognizes that different portions of your money have been invested for different lengths of time, which is the reality of most investment strategies.

In India, mutual fund houses publish CAGR for the scheme (lump-sum view). Your broker/app shows XIRR for your SIP portfolio because you invested in installments.

Common confusion: “My fund says 12% CAGR, but my SIP shows 18% XIRR”. This is normal and correct. XIRR is higher in rising markets because newer installments buy at higher NAVs but still contribute to the final value.

When to Use Which Metric

The best way to understand them is to apply them to specific investment scenarios:

1. Lump Sum Investments

If you invest a single, fixed amount of money and don’t make any further contributions or withdrawals until the end of your investment horizon, CAGR is the ideal metric.

- Example: You invested ₹1,00,000 in a mutual fund and after 5 years, the value is ₹1,80,000. CAGR accurately calculates the average annual growth over that 5-year period.

- Why? The assumption of a single point-to-point investment holds true.

2. Systematic Investment Plans (SIPs)

For SIPs, XIRR is the correct metric. Each installment you invest is a separate cash flow made on a different date, and each stays invested for a different duration. For example, your first SIP installment compounds for the full 5 years, while your last installment only compounds for one month. CAGR completely ignores this complexity, making it an inaccurate reflection of your true SIP experience.

- Example: You start a monthly SIP of ₹10,000. After 3 years, your total investment of ₹3,60,000 has grown to ₹5,00,000. XIRR is needed to calculate the true annualized return by taking the exact dates of each of your 36 installments into account.

- Why? XIRR calculates an annualized return that links all these individual cash flows to the final value.

Key Takeaways in a Comparison Table:

| Feature | CAGR (Compound Annual Growth Rate) | XIRR (eXtended Internal Rate of Return) |

|---|---|---|

| Full Form | CAGR (Compound Annual Growth Rate) | XIRR (eXtended Internal Rate of Return) |

| Primary Use Case | Lump sum (one-time) investments | SIPs, irregular additional investments, or withdrawals |

| What It Assumes | A single investment and a single redemption | Multiple investments and/or redemptions at varying dates |

| Cash Flows Considered | Only the initial and final values | All cash inflows and outflows, along with their exact dates |

| Time Sensitivity | Simple point-to-point duration (e.g., exactly 3 years) | Takes into account the actual duration each rupee was invested |

| Level of Precision | Good for high-level average, not for cash flow-based strategies | Highly precise, tailored to your actual cash flow activity |

| Calculation Method | A straightforward formula | Usually requires tools like Excel or an online calculator (uses an iterative process) |

Important Considerations

- CAGR is not “Wrong,” but it is Limited. CAGR is a valid and useful formula, but it must be used correctly. It’s often used by fund managers to show a fund’s historical performance (e.g., “10-year CAGR”) on a standardized basis, but this should not be confused with your personal SIP performance.

- XIRR Reflects Your Personal Journey. Since XIRR factors in the specific timing of your investments, your personal XIRR can differ from another investor’s, even if you are invested in the same fund for the same total amount, simply because your investment dates were different.

- Look for XIRR on Your Statements. Most modern mutual fund statements and online investment platforms automatically calculate and display the XIRR for your SIP portfolios to provide a more accurate picture of your actual returns.

What about “Absolute Return”?

You might also see “Absolute Return.” This is simply the total percentage change in your investment from the start to the end, without any consideration for the time it took.

It’s a quick, simple measure but it becomes less meaningful for investments held for longer than one year, as it doesn’t give you a standardized way to compare performance over time.

Advantages of CAGR

Extremely simple & easy to understand. Perfect for comparing different investments fairly. Widely used by analysts and fund houses. Great for long-term projections.

Advantages of XIRR

- Most accurate for real-life SIP investors

- Considers exact timing of every rupee

- Shows your personal performance (not just fund performance)

- Handles withdrawals and top-ups perfectly

Limitations

CAGR Limitations:

- Gives wrong picture for SIPs and multiple cash flows.

- Assumes entire money was invested on day one.

XIRR Limitations:

- Cannot be calculated manually (needs Excel or calculator)

- Harder to compare across different investors.

- Changes every time you add new money.

CAGR & XIRR Calculator

Our free online CAGR & XIRR Calculator handles both metrics instantly.

Inputs for CAGR: Initial Value | Final Value | Years Inputs for XIRR: Full list of dates + amounts (or upload CSV)

Results: CAGR %, XIRR %, Total Growth, Doubling Time + beautiful growth chart.

FAQ About CAGR vs XIRR (Most Asked Questions)

Which is better-CAGR or XIRR?

Neither is universally better. Use CAGR for lump-sum & fund comparison. Use XIRR for SIPs and your personal returns. For 95% of Indian investors doing SIPs, XIRR is the correct metric.

Why is XIRR used for SIP returns instead of CAGR?

Because SIPs involve multiple investments at different dates. CAGR assumes all money was invested on day one — which is never true in SIPs. XIRR gives your actual return.

Can XIRR be negative?

Yes. If you invested heavily just before a market crash and haven’t recovered yet, XIRR can be negative even if current value > total invested.

Is XIRR always higher than CAGR?

No. In rising markets XIRR is often higher for SIPs. In falling markets, XIRR can be lower. It depends on timing.

How accurate is XIRR compared to CAGR?

XIRR is more accurate for real investor returns with multiple cash flows. CAGR is accurate only for lump-sum investments.

Can I calculate XIRR without Excel?

Yes — most mutual fund apps (Groww, Zerodha, MF Utility, Kuvera) automatically show your XIRR. Our online calculator also does it instantly.

What is a good XIRR for 5–10 years in equity funds?

12–15%+ is good for large-cap, 15–20%+ for mid/small-cap over long term (after beating inflation ~6–7%).

Should I use CAGR or XIRR to compare two mutual funds?

Use CAGR (the fund’s published returns) for fair comparison. Use XIRR only to compare your own performance in different funds.

Conclusion

CAGR vs XIRR is not a battle — it’s about choosing the right tool for the job.

CAGR gives the clean, comparable story for lump-sum and fund performance. XIRR gives the true, personal story for every SIP investor in India. Now you know exactly when to use each, how to calculate both, and why your numbers never matched before.

Ready to check your real returns? Open our free CAGR & XIRR Calculator, plug in your numbers, and see the truth in seconds.

Stop guessing. Start measuring correctly. Your future portfolio (and peace of mind) will thank you!

Happy investing!